Imagine you’re at a carnival, standing in front of a game like the one shown in Figure 1. One by one, 64 balls are dropped from a chute. As they fall, they bounce randomly left or right off a series of pins—eventually landing in one of seven bins at the bottom.

There are 63 white balls and 1 gray ball. You win a prize if you can correctly guess which bin the gray ball will land in. You win a second prize if you can guess what overall shape the balls will form across the bins once all have landed.

Figure 1. Carnival Game — Actual probabilities of falling in each bin from left to right are: 1/64, 6/64, 15/64, 20/64, 15/64, 6/64, 1/64. Probability literature calls this structure of pins a binomial lattice, where the probability of a ball falling to the left of the pin is 50% as is the probability of a ball falling to the right.

So—

Where do you think the gray ball will land?

What shape do you think will emerge after all 64 balls have dropped?

And if you could only answer one of those two questions, which would you choose? Why?

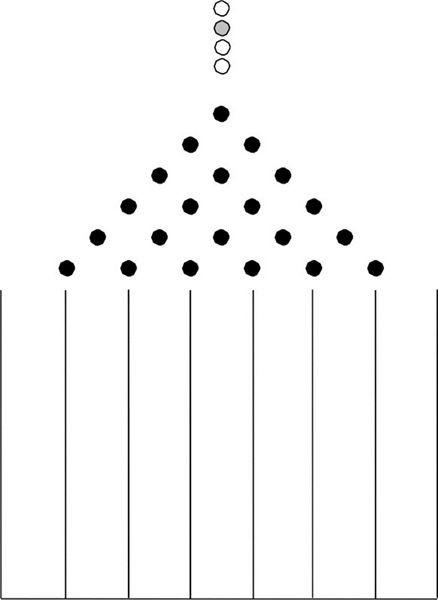

Now take a look at Figure 2, which shows the outcome from a single run of the game.

Figure 2. Outcome of One Trial of the Carnival Game—The device in Figure 2 is alternatively known as a bean machine, quincunx, or Galton box. It was invented by Sir Francis Galton, appearing in his 1889 book Natural Inheritance.

If you guessed the gray ball would land in Bin 3, you were lucky—but you won’t necessarily be right the next time. While the gray ball tends to land somewhere near the middle, on any given run it could just as easily land in Bin 1 or Bin 7. It’s unpredictable.

But the shape the balls form across the bins? That’s a much safer bet.

Across many trials, you’ll see a consistent pattern. The more balls dropped, the more that pattern starts to resemble a classic bell-shaped curve. While there’s some variation from game to game, the overall shape holds.

Your Retirement Security

So what does a carnival game have to do with retirement security?

Plenty.

You can’t predict exactly how long any one person—yourself included—will live. Just like you can’t guess where the gray ball will land in a single trial.

But you can predict the overall survival pattern of a large group of people. And when retirement planning involves pooling individuals together, that predictability becomes a powerful tool.

That’s why lifetime income—like what’s provided by annuities—is so effective. When you spread longevity risk across a large population, the group’s behavior becomes far more predictable.

Take Figure 3, for example. It shows the survival curve for a group of 1,000 females turning age 60 in 2025. While no one woman’s path is known, the group pattern is remarkably consistent—and that allows for planning.

Figure 3. Survivors of Original Cohort of 1,000 Females Turning Age 60 in 2025

The parallel is clear:

- The gray ball represents your individual lifetime—uncertain and unique.

- The overall curve of all balls represents the group pattern—predictable and manageable.

By joining a group that shares longevity risk, individuals gain retirement income security that’s hard to achieve alone. That’s the value of risk pooling, and it’s the foundation behind life annuities.

Arranging the Program to Conquer Longevity Risk

Now, theoretically, any group—your neighborhood association, a church group, even a club—could form their own retirement income pool. But they’d face some tough logistical hurdles.

They’d need someone to:

- Calculate fair monthly income for each person

- Invest the pooled money responsibly

- Administer monthly payments and tax reporting

- Draft the legal agreements

In reality, annuity companies do this work for us. And they do it well.

By operating at scale and across regions, these companies lower costs, improve accuracy, and reduce risks for everyone. They’re regulated, required to maintain reserves, and serve large enough populations that their predictions are more stable – like the pattern of balls in the carnival machine. That stability allows them to build in smaller margins, making the product more efficient and cost-effective for everyone.

Most importantly, they make the process easy. You don’t have to find other participants or build a trust fund from scratch. You just need to choose to participate.

The Takeaway

Extraordinary longevity is not a certainty for which one saves; it is a risk against which one insures.

You don’t hang onto enough money to rebuild your whole house in case of fire—instead, you buy homeowner’s insurance. In the same way, you don’t need to stockpile enough assets to self-fund a life that might stretch to 100. You need a guaranteed income stream that plans ahead against risk and for longevity.

That’s the core difference between:

- A withdrawal strategy, where you draw from a portfolio and hope it lasts; and

- A guaranteed lifetime income strategy, where you know it will.

With the former, you risk running out.

With the latter, you’ve planned for the risk, and you’re ready to reap the reward – a long and comfortable retirement.

Retirement isn’t a practice round. There are no do-overs. The financial choices you make will directly affect your quality of life for decades to come.

The good news? The tools and solutions already exist. You don’t need to invent something new to secure your retirement. You just need to understand the game— and move forward with confidence, not guesswork.

And when the time comes, your future self will thank you.

Jeffrey K. Dellinger, FSA, MAAA, is the author of Another Day in Paradise: The Handbook of Retirement Income, available on Amazon and at retirementincomehandbook.com. The book has been called “a brilliant, clearly articulated picture of what retirement income must accomplish”—and it’s written to guide individuals step by step through one of the most critical financial decisions of their lives.